Setup of the stock – Weak near-term sentiment presents a potentially compelling entry point

AMRT’s stock price has been under pressure due to near-term concerns over macro and margins…

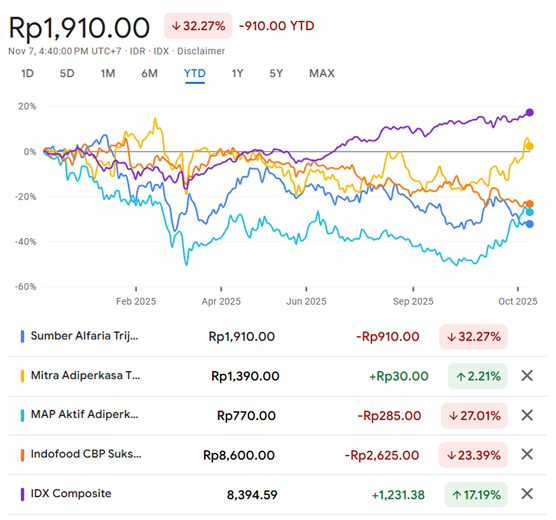

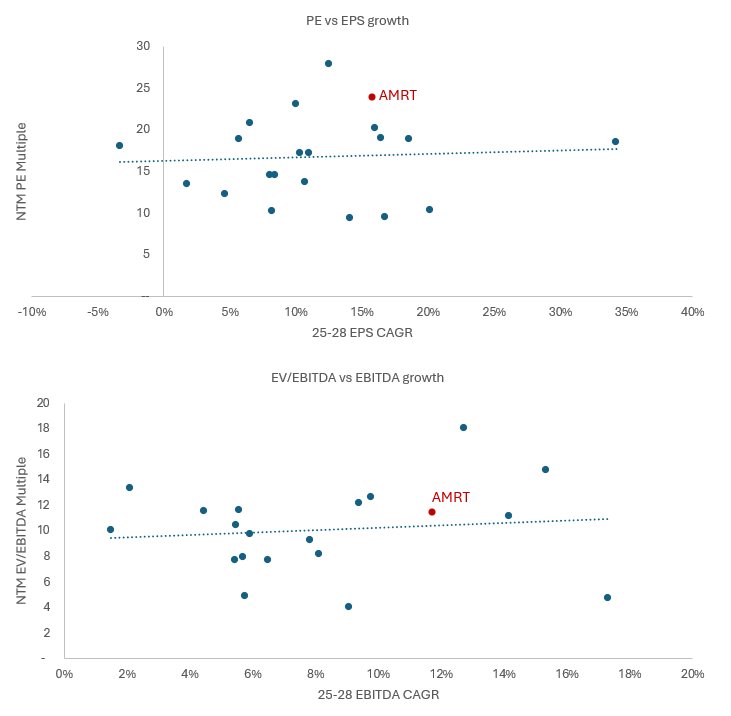

AMRT’s share price remains under pressure (-32% YTD) due to 1) Broader Indonesia consumption weakness, which is affecting all other Indonesian consumer stocks; 2) Concerns over near-term opex overruns from its 3 new distribution centres. NTM Refinitiv consensus PE is depressed at 20.61x (trading c30% below its last 3Y/5Y average of c27x). While the street at face value still looks generally constructive on AMRT (29/30 buy ratings as per Bloomberg), our channel checks with both buyside and sellside analysts indicate that overall investor interest in Indonesia consumer stocks continues to be limited since this year. Overall, AMRT appears to be an overlooked (little foreign flows) and overly punished stock amid these near-term headwinds.

…Yet, AMRT’s longer term story remains intact, making this a potentially compelling entry with favourable R/R

Yet, we believe that AMRT and Indonesia’s longer term consumer growth story (e.g. demographic dividend, emerging middle class, etc.) remains structurally intact. Furthermore, AMRT’s investment in logistics capabilities should further widen its moat in the long run and is the right strategic move for the company, despite the short-term opex overrun pain. As such, this dip in stock price could potentially be an attractive entry point into a high-quality compounder ahead of a sentiment recovery.

Thesis #1 on long term potential – Untapped blue ocean opportunity (esp. ex-Java), despite scepticism that CVS are primarily an “urban phenomenon” and concerns over store unit economics in the more rural ex-Java

Unique geographic conditions in Indonesia (esp ex-Java) make CVS the optimal retail format – offering better pricing and assortment than traditional trade and greater scalability than other modern trade like supermarket

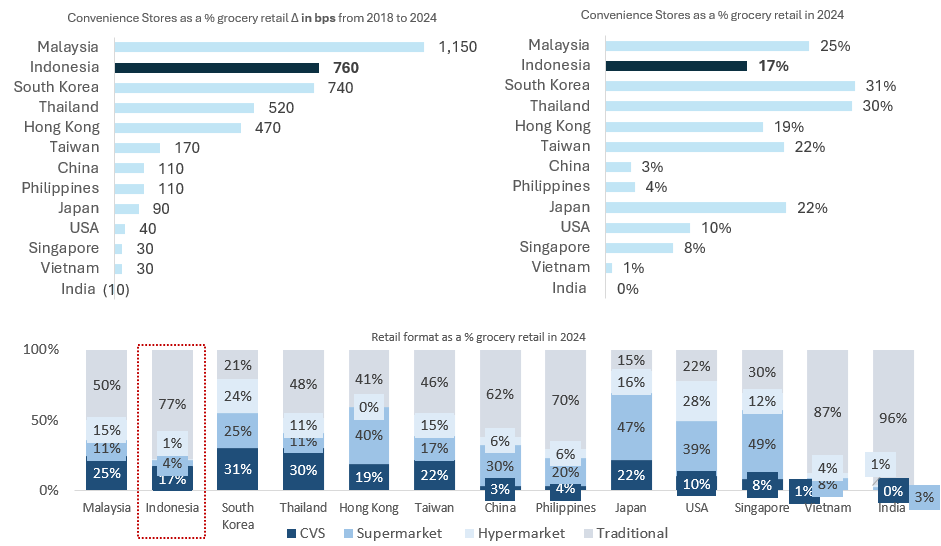

Euromonitor data shows that Indonesia’s CVS share of grocery retail grew 760bps from 2018 to 2024, one of the fastest among our list of benchmark markets. Interesting, this number is now at 17.4%, which is close to many developed East Asian countries (despite their deeply entrenched CVS culture) and much higher than developed markets like Singapore and the US. This supports our hypothesis that CVS is the optimal retail format in Indonesia, countering sceptics (most common pushback based on my conversations with several buyside analysts/PMs and somewhat reflected in relatively conservative consensus store count growth of 5% YoY) who argue they are an “urban phenomenon” and wouldn’t work in the mostly rural Indonesia.

- Modern trade formats like CVS offer better assortment and pricing than traditional trade, leveraging their scale to negotiate more favourable terms with FMCG suppliers than individual shop owners can. Therefore, it is no surprise that modern trade will gradually overtake traditional trade, especially as the market develops.

- Within modern trade, CVS tend to work better than supermarkets and hypermarkets in Indonesia because 1) its 17,500+ islands mean many low-density cities and rural areas (especially outside Java), where larger format retail cannot achieve viable unit economics like in dense urban markets such as Singapore or many US cities. 2) Furthermore, lower purchasing power in Indonesia drives frequent shopping with smaller baskets, a pattern well-suited to CVS formats.

- Some markets like India skipped modern retail and went straight to quick commerce. Indonesia is unlikely to follow the same path in quick commerce because: 1) sufficient density for QC exists only in few Indonesian cities like Jakarta/Surabaya; 2) there isn’t a strong home-cooked meal culture like in India; 3) CVS infrastructure already exists, unlike India’s near-zero modern trade penetration. An Indonesian company ASTRO is already attempting quick commerce but had limited success even in high density cities like Jakarta for reasons above.

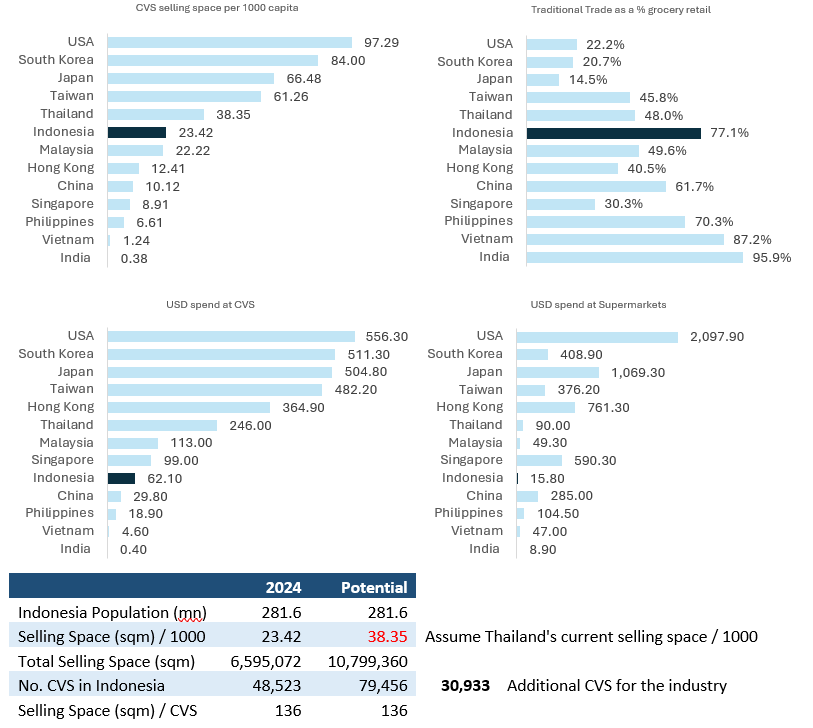

CVS is still a blue ocean opportunity (esp ex-Java) given the high traditional trade penetration to convert into CVS and relatively low selling space per capita

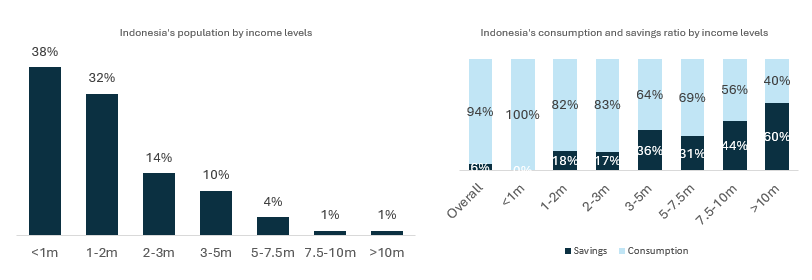

Firstly, Indonesia’s relatively high traditional trade penetration of 77.1%, combined with the price and assortment advantages of modern trade, creates a blue ocean opportunity that has yet to be captured. Secondly, grocery spending remains low in Indonesia due to limited purchasing power (US$62.1 per capita on CVS vs US$246 in Thailand. Most Indonesians still earn <US$120/month). This means significant headroom for growth, benefiting staples especially, if Indonesia can deliver on its economic potential given its vast natural resources and young workforce. A back-of-the-envelope calculation using Euromonitor data can help quantify this potential.

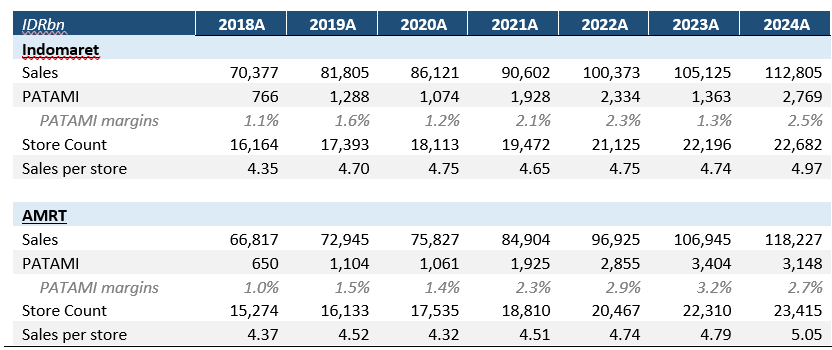

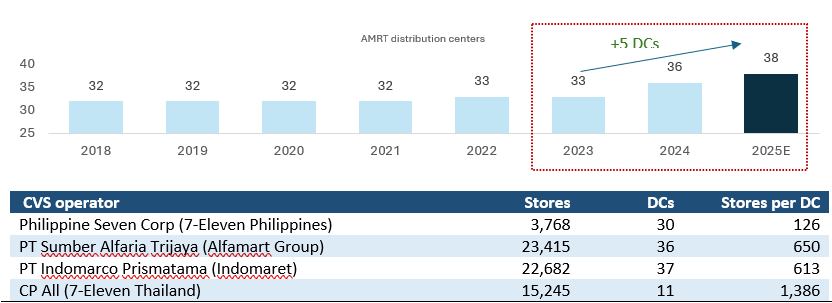

- Assuming that Indonesia’s selling space per 1,000 capita can Thailand’s levels at some point in the future, this means an additional 30,933 CVS for the industry (i.e. +67% in no. stores), assuming population is constant to simplify calculations. For context, AMRT only has 23,415 while Indomaret has 22,682 stores in 2024.

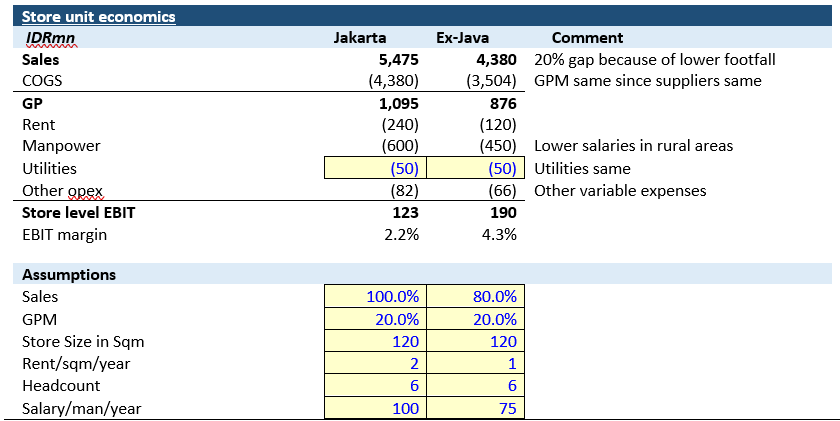

Contrary to sceptics, ex-Java expansion opportunities can have better store unit economics than even in Jakarta primarily because of lower operational expenses.

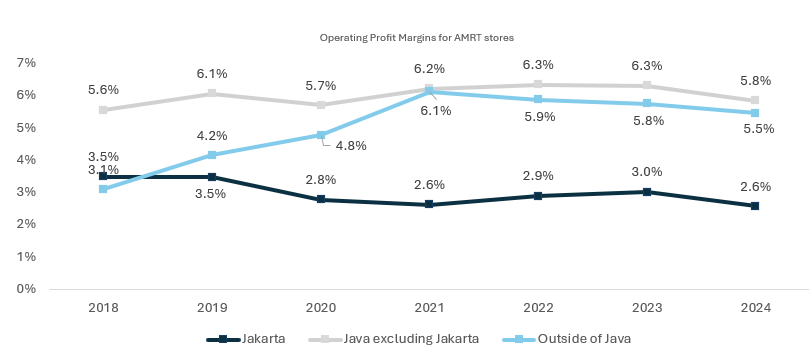

Most expansion opportunities lie outside Java, where areas are more rural (lower store traffic) and purchasing power is lower (spend on lower margin items or lower basket size), raising concerns about weaker store unit economics and potential margin dilution. However, preliminary research and channel checks with Indonesian contacts (note: this is very preliminary given lack of access to contacts) suggest that CVS unit economics outside Java could be stronger than in Jakarta, because of lower operational costs such as rent and labour. An illustrative example is provided below, and assumptions can be adjusted in the attached model under the “CVS UE” tab. Moreover, as of 2024: ex-Java AMRT stores OP margins are at 5.5% vs Jakarta at 2.6% and Java 5.8%.

Thesis #2 on competitive moats – A favourable market structure, coupled with solidifying logistics moat and growing supplier bargaining power, positions AMRT well to capture the blue ocean opportunity ahead

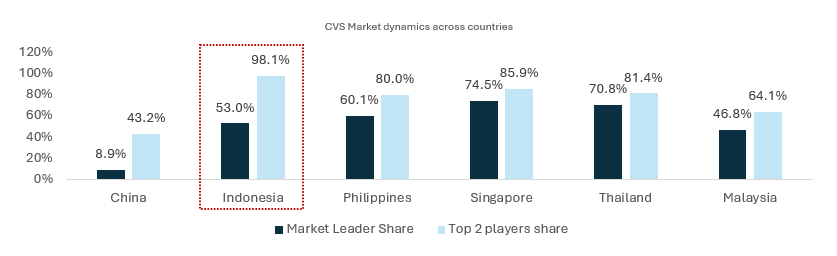

Duopoly market structure in Indonesia CVS discourages irrational competition, though also means difficulty in taking market share

Unlike consumer tech sectors such as e-commerce or online food delivery, competition in Indonesia’s CVS market is relatively benign. This is likely because of a duopoly structure, where the two players have very similar market share and unit economics and rather coexist than engage in a zero-sum battle. Additionally, minimal differentiation between Alfamart and Indomaret, coupled with the need for each store to reach a minimum profitable volume, means opening near a competitor offers little advantage if local density is insufficient, discouraging irrational competition. Finally, the market’s large potential as explained above also reduces incentive for a cutthroat battle. All that said, this also means that it will be difficult to grow by taking market share, and growth will primarily be at the back of overall market growth.

AMRT is increasingly building a structural cost advantage driven by its 1) expanding logistics network; 2) improving supplier bargaining power because of its increasing scale

Indonesia’s supply chain infrastructure remains broadly underdeveloped, particularly outside Java and major urban centres. Against this backdrop, Alfamart’s logistics network acts as a key competitive edge and barriers to entry by ensuring product availability and efficient inventory management across the archipelago. To improve supply chain efficiency and lower long-term logistics costs, AMRT added 3 new distribution centres (DCs) in 2023 to 2024 and plans to complete 2 more in 2025. This expanded DC network further solidifies its logistics moat, allowing it to reduce logistics cost and support AMRT’s stored expansion especially outside of Java.

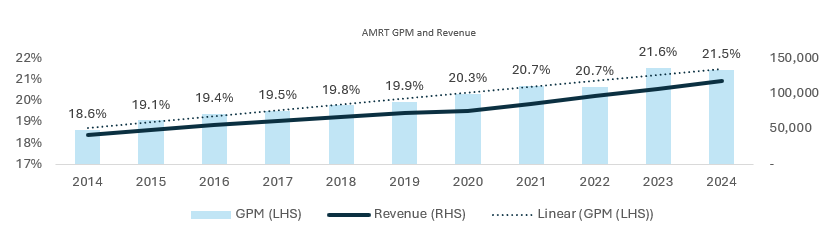

There is a strong correlation between revenue and GPM (Fig. 10), likely because as AMRT scales, it gains greater negotiating power with suppliers and can thus lower costs. The larger AMRT grows across Indonesia, the more it can either offer lower prices to customers or capture higher margins if it chooses not to pass on cost savings. Given Indonesians’ general price sensitivity, this provides a meaningful competitive edge and barriers to entry. It is important to note that there will be QoQ fluctuations in GPM, and it won’t expand in a straight line. Given our longer-term investment horizon, we choose to focus on YoY GPM trends, which shows an almost consistently upward trajectory.

Thesis #3 on financial health – Prudent capital structure, along a profitable and cash-generative business model, puts AMRT in a good position to 1) expand aggressively via debt; 2) cash buffer to weather unexpected storms

AMRT has deleveraged over the years (now net cash ~US$195 mn) thanks to strong operating cash flow and prudent capital allocation. This provides ample headroom to deploy internal cash, or load up on debt if needed (cheaper forms of capital vs equity), to accelerate ex-Java expansion. Otherwise, this strong balance sheet also acts as a buffer in case of emergencies. That said, there is still much profitability and cash generation are below peers (e.g. CP All OCF as a % revenue is at 7.71% while Philippine Seven is at 15.4%), meaning that there is still room for optimization. Our concern though is that I am getting the impression that management doesn’t seem to be risk taking enough and appears to be generally more conservative.

Risks, where could go wrong, catalysts and further due diligence needed to build conviction

Risk #1: CVS TAM outside Java is not as big as anticipated, or AMRT is unable to penetrate ex Java in a meaningful manner

- Firstly, existing customers may still prefer traditional warungs due to familiarity and social bonds.

- Secondly, while some UE analysis was conducted, our assumptions are admittedly not very tight/high conviction. Lower-than-expected footfall from low population density along with lower basket sizes could undermine UE, while higher than expected opex may arise from reduced economies of scale in delivery, advertising, and management overheads.

- Thirdly, we may also have overestimated the TAM outside of Java. Ideally, we should look into each cities in Java and consider population density, logistics efficiency, and local purchasing power to do a bottom-up market sizing.

- Mitigation: All that said, CVS have proven to successfully expanded into smaller towns in countries like Japan, Taiwan and Thailand, due to dense logistics networks, strong brand trust, and consistent service quality – although, “rural” in these countries often still implies relatively high population density

Risk #2: E-commerce could undercut offline prices, prompting consumers to shift online

- E-commerce platforms such as Shopee have been investing heavily in their logistics networks, along with a strong emphasis on price competitiveness. Being well capitalized, these platforms can afford to subsidize costs over an extended period, allowing e-commerce platforms to undercut AMRT’s pricing and potentially permanently shift consumer behaviour from visiting physical convenience stores to purchasing online.

- Mitigation: That said, e-commerce delivery still takes at least 2 to 3 days, especially in rural areas. Given AMRT’s ability to offer slightly lower prices, since it does not bear the added logistics cost of doorstep delivery, this risk is quite mitigated. AMRT has also gone into e-commerce via Alfagift, though traction remains limited.

Risk #3: Unexpected macro headwinds would impact AMRT’s earnings

- Indonesia has long been seen as a country with immense potential, given its young, sizable population and abundant natural resources. However, it seems like realizing this potential is very challenging, in our view due to persistent issues of KKN (Korupsi, Kolusi, dan Nepotisme). We may hence overestimate Indonesia’s longer term growth story and modelled unrealistic TGR/SSSG. Other unexpected macro events (e.g. recent Trump liberation day, China’s slowdown leading to less demand for commodities, Vietnam attracting textile factories over from Indonesia, etc.) may also impact AMRT.

- Mitigation: Strong balance sheet would help buffer such impact, and cushion some value destruction from macro events, which we simply cannot predict.

Risk #4: Unexpected regulations may impact AMRT’s earnings

- For instance, raising minimum wages would significantly impact manpower cost

- Mitigation: Efforts to automate processes in the future, along with expanding margins from scale can help mitigate this.

Catalysts and datapoints to watch out:

- Monthly BI data on retail sales index and consumer confidence index

- Indonesia consumer stocks quarterly earnings and guidance

- More datapoints or news flow on success of its ex-Java penetration (store count, SSSG), along with improving margins (GPM, Opex as a % sales) and more dividends/buybacks

Additional due diligence needed:

- I would like to conduct more on-the-ground checks with consumers in rural areas outside Java to better understand their consumption habits and validate our thesis on long-term expansion opportunities in ex-Java. So far, our insights are only based on a few urban-based Indonesian friends (Jakarta, Medan, Surabaya) and a former family helper from Manado (Sulawesi, ex-Java).

- I also hope to speak with AMRT franchise owners or company management to gain a clearer picture of store-level unit economics in both Java and ex-Java, which would help test the idea that ex-Java store economics are not necessarily worse than in Java. Additionally, what levels of logistics, purchasing power and population density are required to make UE work.

- I am also not too satisfied with our current work on logistics benchmarking. It is difficult to find disclosures on logistics across CVS, so I think speaking to a logistics expert would help in better understanding how good AMRT’s logistics network truly is as of now vs global benchmarks.

- Since much of the supporting data comes from Euromonitor, I aim to consult Euromonitor’s sector team to understand how these figures are estimated. I also want to explore alternative databases for cross-referencing and potentially conduct our own market sizing.

- Admittedly, the core of our time was spent on understanding the Indonesia CVS landscape. However, better understanding case studies from across the world would also help in building a more differentiated investment case. More comparison of AMRT with other global peers – e.g. in logistics capabilities, in product mix, margin profile, etc.

- More due diligence and comparison with other Indonesian consumer stocks to better understand the premium that investors place on AMRT vs other Indonesian consumer stocks which are also beaten down.

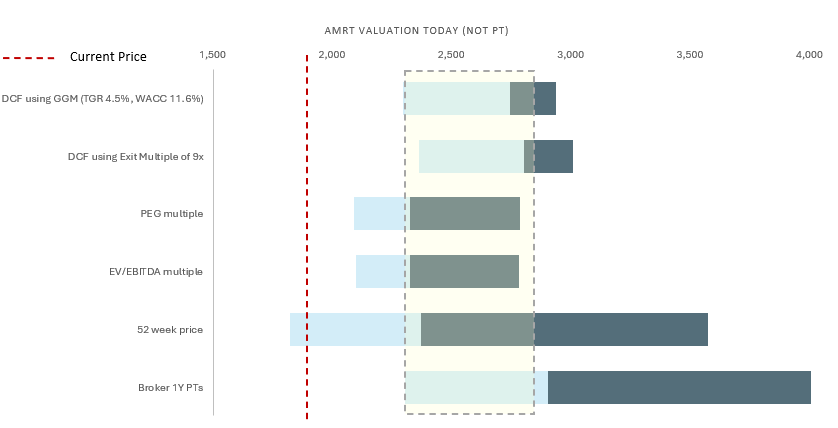

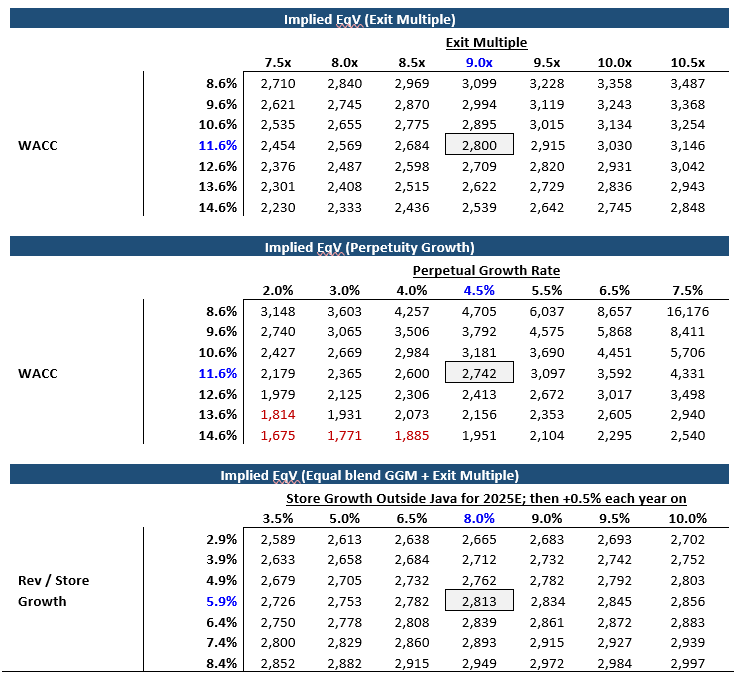

Valuations – 3Y price target of Rp3,400 representing 15.4% IRR

Valuation Overview: We arrive at a 1-year PT of rp2,800 and 3-year PT of rp3,400 (+21.2% IRR) by using an equal blend of 1) income approach via DCF with both Gorden growth and exit multiple method and 2) market approach via consensus PEG of Indonesian consumer peers. We used a DCF to capture our view on AMRT’s ex-Java expansion and margins trajectory, while using PEG to reflect current market sentiments on the Indonesian consumer sector.

Market Approach: The PEG ratio was used to account for differing growth profiles across the comparable set. The analysis focused on Indonesian consumer stocks (added the main Indonesian consumer stocks with enough consensus estimates for reliable forward multiples), which better reflect AMRT’s value, as they share a more similar investor base than regional CVS operators. PEG of 1.48x was used.

Interested in the full investment case and want the excel copy of our full model?

You can purchase the institutional-grade Alfamart valuation model and complete stock pitch used in this deep dive, featuring a fully integrated 3-statement financial model, DCF, comps analysis, and detailed, transparent assumptions. Your support directly helps fund Skeptivest’s independent, in-depth research, enabling us to continue publishing high-quality fundamental analysis like this.