Set up – Re-rating driven by better fundamentals and “Capital Return Programme”; Stock currently supported by retail buying

The stock price has doubled since 2024, driven by a combination of better fundamentals and corporate actions.

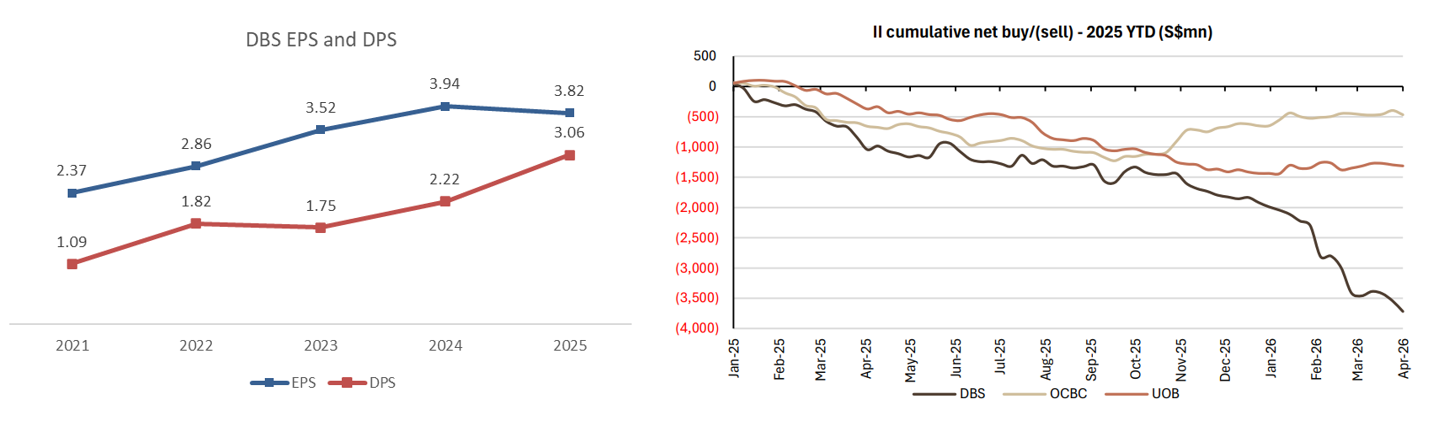

- Record EPS increased from 3.52 to 3.94, accompanied by higher DPS growth from 1.75 to 2.22.

- Wealth management has also emerged as a structural growth engine (+28% 2022-25 revenue CAGR)

- DBS benefitted from a higher interest rate environment (e.g. NIMs up from 2010-19 avg of 1.77% to >2% from 2023, although we are starting to see NIMs normalize down as SORA declines)

- “Capital Return Programme”, under which:

- DBS plans to return S$5bn in “capital return dividends” from 2025-27. Payout ratio increased from 56% in 2024 to 80% in 2025 because of this.

- Alongside a S$3bn share buyback.

- Many other Singapore stocks seems to be doing "value unlock" initiatives like this - e.g. Singtel's "Value Realization Dividend and Share Buyback"

Flow wise, the stock appears to be supported largely by retail buying, as institutional investors have continued to be net sellers of DBS shares throughout the year, as per SGX data. We think institutional investors are likely concerned that valuations have become stretched, while record earnings achieved in recent years (driven by being in a higher interest rate environment) are likely to normalize over time as SORA decline. However, the stock has continued to hold up (stock is still up 6.7% YTD) as retail investors keep adding, which we believe is largely due to the stock’s still-attractive dividend yield.

Is DBS still attractive at current valuations? – We think so from a dividend yield lens

We would focus on dividend yield, given that retail buying seems to be the primary driver of the stock price currently (DBS is viewed as a dividend stock and hence dividend yield is a key metric to watch by retail investors). Overall, we think retail buying on attractive dividend yield would continue to support the stock price.

- Dividend yield is at 1) 5.57% on NTM consensus DPS; 2) 4.19% on last financial year DPS.

- This remains attractive vs cut off yield for the latest 1-year Singapore T-bill of 1.46%, Singapore Savings Bond of 2.11%, and Singtel’s 4.43% yield on NTM consensus DPS (Note: We benchmark against Singtel because it is another blue-chip dividend stock that retail investors are likely to compare against. Singtel should trade at a slightly lower yield given it is more defensive against macro risks)

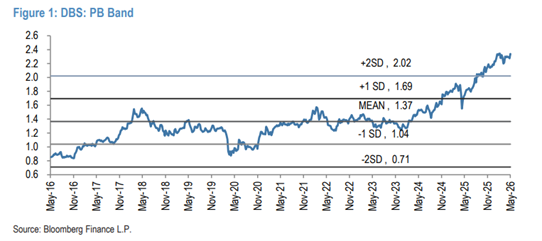

However, from a P/B perspective, valuations do look stretched at 2.4x especially when compared with historical 10Y mean of 1.37x. Compared to peers, DBS is trading at a c45% premium to OCBC on a P/B basis, which looks high but is in-line with 5Y historical mean. All that said, this is partly justified given better earnings, more capital return to shareholders and the broader Singapore market re-rating from the government’s efforts to revive the equity markets (e.g. EQDP). We also think this is metric is less emphasised by retail investors.

Earnings could moderate as we enter into a lower rates environment (lower NII/NIM) + tough macro (higher credit cost, lower loan growth), but dividend visibility until at least 2027 should continue to support the stock

Earnings / EPS could moderate going forward given: 1) NIM expected to trend down from 2024 highs (higher rate environment then) as SORA decline as we go into a lower rate environment; 2) credit cost could increase given the current tough macro; 3) loan growth could be impacted as business sentiments deteriorate from macro risks. That said, this could be offset by fee income from wealth management which continues to benefit from redirection of net new money from the middle east towards Singapore.

Dividend / DPS visibility at least until 2027 seems pretty set with the capital return programme and hence should not be a major source of upside/downside risk concern. However, this also suggests that dividend yields could come off after 2027 once the programme concludes. Clarity on DPS going into 2028 is important to monitor as it can potentially have material implications on dividend yield (and hence a reason to potentially sell).

Overall, we think DBS remains attractive...

Overall, we think DBS remains attractive despite the recent re-rating and some potential near-term sources of negative surprise from tougher macro, given its relatively high forward dividend yield (primarily due to its capital return programme) and the overall quality of the business. Retail should continue to support the stock even with institutional net sell. Furthermore, Singapore’s push to revitalise the equities market via the EQDP could also provide support for DBS, given that it accounts for roughly a quarter of the STI and not a stock institutional money can ignore when benchmarked against and allocating to Singapore equities.