Backdrop – After a ~30% rally in 2025, Hong Kong now faces a struggling equity market

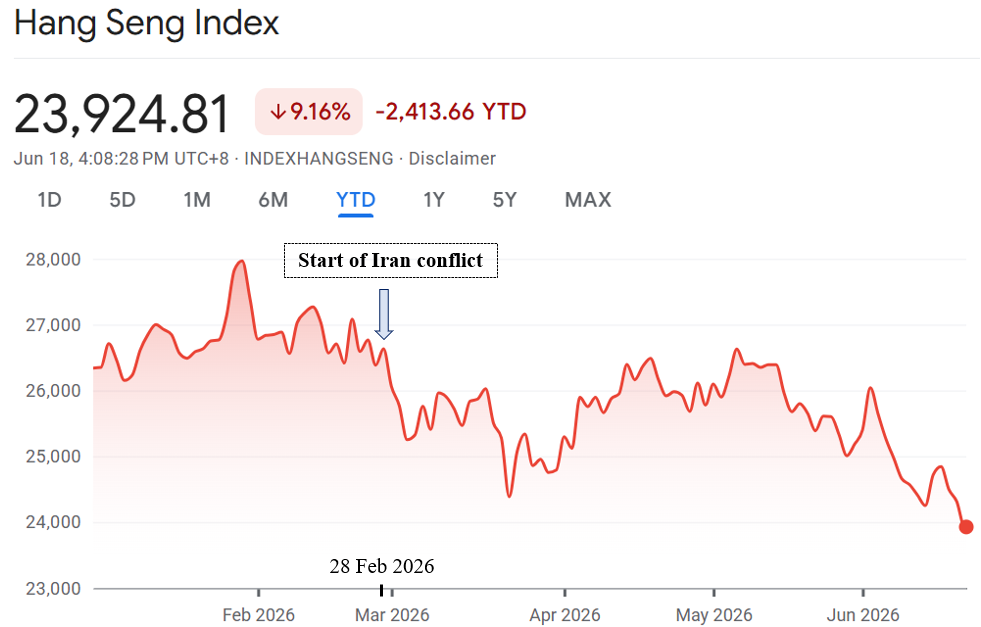

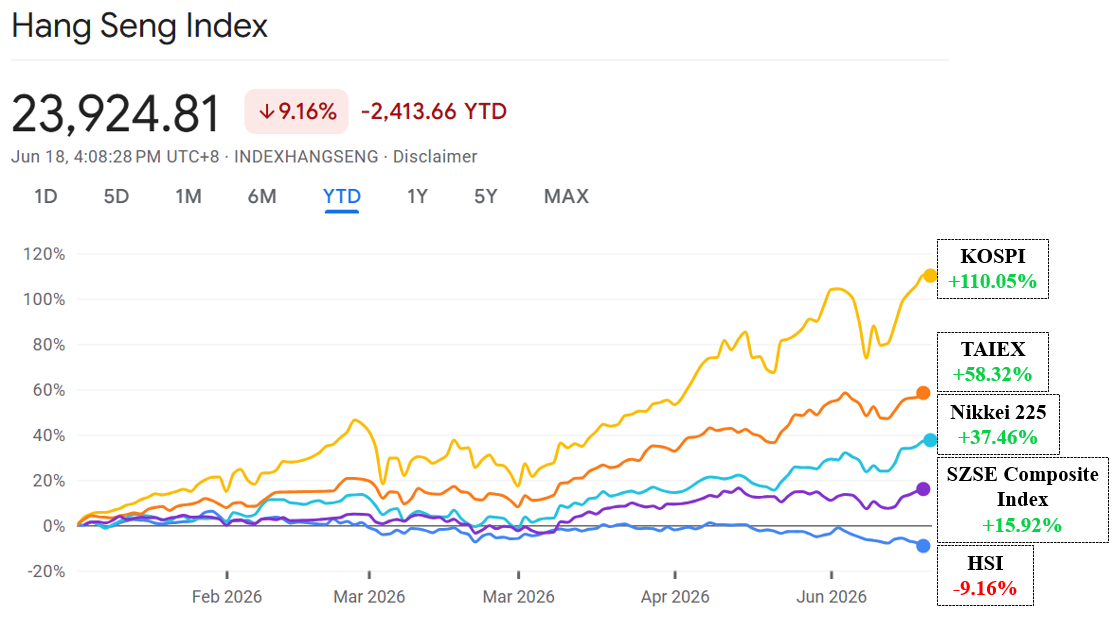

The Hang Seng China Enterprises Index (HSI) is now down 9.16% year-to-date. This is particularly striking given the resilience seen across other Asian equity markets, including China, Taiwan, South Korea and Japan.

The HSI’s performance is underwhelming by any standard. As the main benchmark of the Hong Kong stock market, it comprises up to 100 of the largest and most liquid companies listed on the Stock Exchange of Hong Kong.

Historically, Hong Kong-listed Chinese companies (H-shares) tend to struggle under the following conditions:

(1) A surging US dollar (USD)

A strong USD tends to:

- Reflect broader US economic growth and outperformance, drawing capital away from emerging markets and into US assets.

- USD strength also typically puts downward pressure on the RMB, raising concerns over currency depreciation and reducing the value of Chinese corporate earnings in USD terms.

- In addition, Hong Kong's Linked Exchange Rate System effectively imports US monetary policy into the local economy. Because the HKD is pegged to the USD, a stronger USD, typically associated with higher US interest rates, tends to be accompanied by higher interest rates in Hong Kong as well. This raises borrowing costs, weighs on property and equity valuations, and can negatively affect sectors that make up a significant portion of the Hong Kong market, including property developers, banks, and consumer-related companies.

Yet, while the greenback remains relatively strong today (DXY = 100.85), it has not appreciated materially over the past 12 months. Moreover, the easing of tensions surrounding the Iran crisis could pave the way for further USD weakness as global investors look to rotate out of safe haven assets and rebalance capital away from US assets.

(2) Weak Chinese equity markets

Yet, this is clearly not the case. In USD terms, the Shanghai Composite Index has gained 28% over the past year, while the Shenzhen Composite Index has risen an even stronger 43% in the past year.

Weak Chinese equity markets often translate into weak Hong Kong equities because both are closely tied through earnings exposure, sentiment, and capital flows. Many H-shares derive significant revenue from mainland China, so weaker A-share performance typically signals softer growth and earnings expectations. At the same time, mainland equities act as a key barometer of China’s macroeconomic outlook, meaning that weakness in China's growth tends to dampen overall risk sentiment toward Chinese assets.

(3) A deteriorating Hong Kong property market

However, this year, we have seen improvements across key indicators, with transaction volumes, property prices, and rental yields all trending higher. The sector appears to be gradually recovering from the 2021-2025 post-peak slump, where the market experienced a major downward correction.

During that period, residential property prices in Hong Kong entered a sustained downturn in 2021 after a prolonged boom, with lived-in home prices declining for three consecutive years through 2024, the longest losing streak since the aftermath of the Asian Financial Crisis. The correction was driven by a combination of elevated interest rates, weaker economic growth in mainland China, and a post-pandemic oversupply of new housing. With these pressures beginning to ease, Hong Kong’s property market now appears to be stabilising and gradually recovering.

(4) Political uncertainty in Hong Kong

Over the past decade, Hong Kong has weathered two major periods of instability, namely the 2014 Umbrella Movement and the 2019 Anti-Extradition Bill protests, which weighed on consumer, business, and investor sentiment. Today, however, there are few signs of contentious social issues and political tensions; Hong Kong’s political environment appears calmer than it has been for much of the past decade.

In short, none of the traditional headwinds typically associated with weak H-shares’ performance appear sufficient to explain the lacklustre performance of Hong Kong equities today. The puzzle is that some of these usual headwinds appear less severe, yet H-shares have still lagged, suggesting other factors that may be playing a larger role in this environment.

Why Mainland Chinese stocks are outperforming their Hong Kong listed peers

A likely explanation for the divergence is tighter restrictions on capital outflows from China

Beijing has increasingly signalled a preference for keeping domestic savings onshore, and the scrutiny of several Singapore and Hong Kong-based online brokers, namely Futu, Tiger Brokers and Long Bridge Securities, in late-May reinforced concerns that authorities are becoming more vigilant about cross-border capital movement (China targets offshore billions in biggest crackdown in decades). This stance may be driven in part by fears of capital flight as domestic interest rates continue to decline. At the same time, Chinese policymakers may also be seeking to generate a positive wealth effect domestically, in order to support consumer confidence, particularly among urban millennials and Gen Z, who have suffered from elevated youth unemployment and falling property prices. In this regard, supporting A-shares performance, whether in Shenzhen and Shanghai, is likely to be prioritised over H-shares, which are predominantly held by foreign investors and therefore have less direct impact on domestic sentiment and spending.

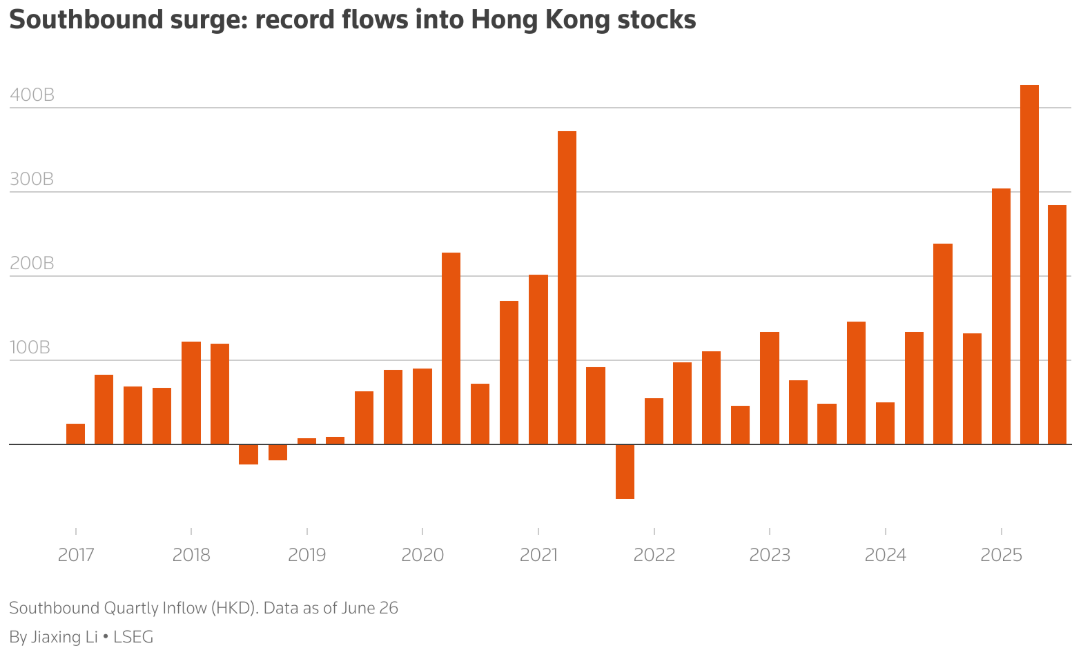

The RMB exchange rate has long influenced Chinese investment flows into Hong Kong, but this dynamic is now shifting

Another possible explanation is the role of the RMB exchange rate in shaping Chinese investment flows into Hong Kong. In the past, when the RMB was depreciating at around 3% annually against the USD in 2022, there was a strong incentive for capital to move offshore. Once in Hong Kong, funds could be placed into USD time deposits or USD-linked insurance products yielding ~5%. Combining the interest incomes with the annual US dollar gains of around 3%, effectively generated total returns of around 8% in RMB terms, at a time when domestic inflation was essentially negative. This made Hong Kong an attractive destination for Chinese savings seeking stable, high real returns with relatively low volatility. Historical capital flows reflected this dynamic (Chinese investors pour record funds into Hong Kong stocks in first quarter).

However, this “easy carry” has largely disappeared. The RMB has since shifted from steady depreciation to periods of stability or even appreciation, while USD deposit yields have also fallen from ~5% to closer to 3.5%. As a result, the previous positive return differential has not only compressed but potentially reversed, with lower offshore yields and less favourable currency dynamics reducing the appeal of moving funds into Hong Kong. In short, the incentives that once supported strong capital inflows into Hong Kong are no longer present to the same degree.

Index composition may also explain the divergence between the two markets

Compared with Shenzhen, which has greater exposure to the tech hardware names that have performed strongly in 2026, Hong Kong’s H-shares index is more heavily weighted towards large internet platforms such as Alibaba, Tencent, Meituan, Baidu, and JD.com. These stocks have lagged as investors rotate away from internet names, amid concerns around regulatory overhang and heavy AI-related capex that has yet to translate into earnings, and into hardware and semiconductor-related companies that are more directly leveraged to the AI investment cycle. Investors are increasingly pivoting away from Hong Kong-listed tech giants toward Mainland-listed semiconductor and AI-related shares, viewing them as more immediate beneficiaries of growth. In this sense, Hong Kong has effectively become a source of funding for this rotation rather than a beneficiary of it. Recently, southbound investors are also frequently seen as treating rallies in Hong Kong-listed tech companies as opportunities to cash out, further exacerbating the sell-off on Hong Kong stock exchange (Chinese investors exit Hong Kong stocks as AI woos money onshore).

Without any clear catalyst, the outlook for Hong Kong stock market remains challenged in the near-term

None of the prevailing explanations fully account for the underperformance

Admittedly, none of the above explanations appears sufficient to justify the extent of Hong Kong’s recent weakness. More broadly, the Hong Kong equity market is beginning to show signs of weakness at a time when domestic macro conditions are arguably the strongest they have been in years, supported by a robust IPO pipeline, a stabilising property market, and a government that appears to be delivering reasonably well on voters’ expectations. Yet, despite reasonable fundamentals, ample liquidity, and attractive valuations, momentum continues to deteriorate, which is increasingly the source of concern.

Impending wave of massive stock lock-up expiries

Looking ahead, Hong Kong’s equity market is set to face renewed downward pressure as approximately HK$255 billion (US$32.5 billion) of post-IPO lock-up restrictions expire in July 2026, triggering a significant surge in potentially tradeable supply (Hong Kong market faces pressure as HK$255 billion in locked shares expire in July). This wave of expiries stems from the IPO boom in late 2025 and early 2026, when a large number of Chinese technology and AI startups rushed to list in Hong Kong amid strong investor enthusiasm for the AI theme, marking the city’s strongest fundraising quarter since 2021 with nearly US$14 billion raised.

Under Hong Kong’s standard six-month lock-up rules, cornerstone investors, insiders, and pre-IPO shareholders are now reaching the end of their selling restrictions simultaneously, creating a concentrated unlock event. Companies contributing to this wave include recent high-profile listings such as AI model developer MiniMax Group and Knowledge Atlas Technology (Zhipu). Given that many early investors entered at very low valuations, the expiry of the lock-up period creates a strong incentive to take profits, raising the risk of a meaningful supply overhang in the near term.

Trade Idea: Long mainland A-shares (CSI 300 / SZSE Composite) vs Short HSI

We prefer to stay cautious on Hong Kong equities and express a relative value view by going long mainland A-shares (CSI 300 / SZSE Composite) versus short the HSI. Onshore markets appear better positioned in the near term, supported by a more constructive policy and liquidity backdrop, alongside more direct exposures to semiconductors and the broader AI investment cycle. A-shares also screen more attractive from a positioning and valuation perspective, and have yet to become overly stretched, offering a more favourable risk-reward profile.

In contrast, Hong Kong equities remain vulnerable to near-term technical and supply overhangs. In particular, the upcoming wave of post-IPO lock-up expirations could introduce meaningful supply pressures as investors look to offload their locked shares, potentially triggering another leg of sell-off. Combined with recent underperformance and already subdued investor positioning, this reinforces a more cautious stance on H-shares. Overall, we see this as a compelling relative value and event-driven opportunity, favoring long mainland A-shares versus short HSI.