Backdrop – Persistent rupiah weakness further exacerbated by Middle East conflict, prompting BI intervention

IDR has been down ~5% against the USD since the start of the Middle East conflict. The currency has come under intense pressure amid elevated oil prices, rising inflation concerns, a stronger USD, and tighter global financial conditions. A subdued domestic growth outlook has also dampened market sentiments and weighed on capital flows into the country.

BI is taking little comfort in IDR's depreciation to current levels and has already implemented several measures to manage the pressures.

- FX intervention: Direct intervention in the FX market around the clock via FX reserves

- SRBI: Raising SRBI yields to attract capital inflows and support rupiah demand; higher yields on SRBI and SBN have helped revive foreign portfolio inflows in 2Q26

- SBN: BI’s purchase of SBN in the secondary market to maintain monetary-fiscal coordination

- Maintain domestic liquidity: Ensure that banking system liquidity remains sufficient through reserve requirement cuts and continued money market injections

- Tighter restrictions: A limit on dollar purchases without underlying assets lowered to USD25,000 from USD100,000

- NDFs: Allowing domestic banks to participate in selling offshore non-deliverable forwards (NDFs)

- Tighter oversight: Coordination with the Financial Services Authority (OJK) to oversee high dollar purchasing activity

Yet, despite these measures, the IDR has continued to depreciate against the USD and underperform its peers. On 8 May, BI reported that gross FX reserves fell from US$148.2bn in March to USD146.2bn in April due to government external debt repayments and FX stabilisation measures, equivalent to 5.8 months of import coverage. A further drawdown in FX reserves heightens concerns over FX reserve adequacy, and hence the ability of the central bank to conduct FX intervention and maintain currency stability.

An all-out approach to restore FX stability and mounting economic pressure has, instead of reassuring markets, left investors in jitters

(1) A whopping 50bps rate hike catches markets off guard

On Thursday, BI unexpectedly raised its policy rate by 50bps to 5.25%, ending a seven-month pause, as it moved to defend the rupiah and pre-empt inflation risks amidst sharp FX depreciation and a narrowing US-Indonesia interest rate differential.

Expect more policy surprises ahead – Markets are now pricing in further rate hikes in the coming quarter. Oil prices, a key factor contributing to inflationary pressures and the IDR weakness, are expected to remain elevated above US$100 per barrel in the near term. Should rupiah sustain its depreciation momentum, I think that BI is likely to prioritise USDIDR stability even at the expense of growth. That said, a de-escalation in the Middle East conflict, which could ease pressure on the IDR, may allow BI to temporarily look through the currency weakness and adopt a wait-and-see approach before considering further rate hikes.

Rate hikes to defend the IDR, but at what cost? – Despite an all-out response to stabilise the rupiah, the IDR has continued to depreciate against the USD, which ultimately prompted BI to hike rates. Yet, the tightening cycle is likely to come with growth trade-offs, as higher rates weigh on domestic demand and investment activity.

(2) A commodity export shake-up: Centralising exports under Danantara's oversight

In an attempt to contain currency and fiscal weakness, President Prabowo further announced this week that Indonesia will centralise exports of key commodities, including coal, palm oil, and ferroalloys, under a designated state-owned enterprise, managed by Danantara, Indonesia’s sovereign wealth fund. As the world’s largest exporter of these commodities, Indonesia is seeking to retain more export earnings onshore, with Prabowo framing the decision as a way to “prevent earnings being held offshore”, curb under-invoicing, transfer-pricing and embezzlement of export proceeds, which have contributed to the low revenue-to-GDP growth of 11%. This comes as the government reiterated a fiscal deficit target of 1.8%–2.4% of GDP, underscoring its focus on fiscal discipline amid external pressures.

However, markets reacted defensively to the news, with the Jakarta Composite Index falling ~2.4% as tighter oversight of commodity exports fueled concerns over greater state control and weaker profitability.

The pattern of sudden policy shifts may be a “boon” for country, but a bane for investors

(1) Weakening macro fundamentals continue to weigh on Indonesian equities

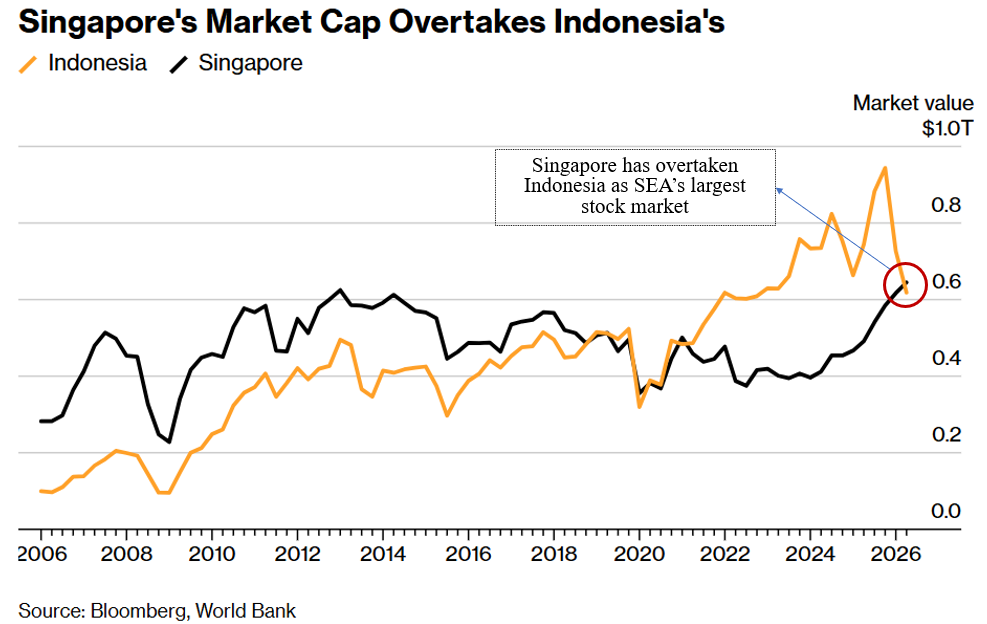

According to recent data compiled by Bloomberg, Singapore has now overtaken Indonesia as SEA’s largest stock market, with market capitalisation rising to US$645 billion, while Indonesia’s has declined over 30% from its January peak to US$618 billion (Link). This divergence in equity performances can be attributed to several factors.

Reclassification risks and credit rating concerns – Investor sentiment towards Indonesian equities has deteriorated amid uncertainty over equity reclassification and credit rating outlook downgrades, while Singapore stocks have benefited from relative economic stability and government-led efforts to revitalise its market through the Equity Market Development Program.

Currency moves have also played a part, with rupiah weakness weighing on Indonesian assets while the Singapore dollar has strengthened following tighter monetary policy by MAS at its April meeting.

(2) Amid the volatility and sell-off, we prefer to stay cautious given the headwinds ahead

Investors should caution against rushing to buy the dip – While the government has under taken an all-out effort to support currency stability, caution remains warranted given ongoing policy uncertainty and weakening macroeconomic fundamentals. I think that beyond the market impact, the abruptness and frequency of regulatory changes are a greater concern, signalling rising regulatory risk. So far, the Indonesian government does not have a strong track record in turning things around. Equity valuations will continue to price in a higher regulatory discount. Near-term risks around FX stability, higher interest rates, and slowing growth are also likely to keep sentiment subdued until macro conditions stabilise, which in turn remains partly dependent on other external factors as well, such as developments in the Middle East conflict.

(3) That said, we see select undervalued opportunities in the sell-off...

Bank winners from higher rates and FX liquidity shift – The big banks, particularly Bank Central Asia, may be well-positioned to benefit from a higher interest rate environment and lower reserve requirements, which supports net interest margins. State-owned lenders such as Bank Mandiri may also see incremental inflows of USD liquidity under the new DHE regulation, alongside potential upside from increased trade finance and exporter-related flows. Hence, we see value in buying the large-cap bank names on retracement, particularly through long positions in Bank Central Asia (IDX: BBCA) or Bank Negara Indonesia (IDX: BBNI). Blue-chip Indonesian banks are currently trading at more attractive valuations following the broader market sell-off and are well positioned to benefit from BI intervention measures.